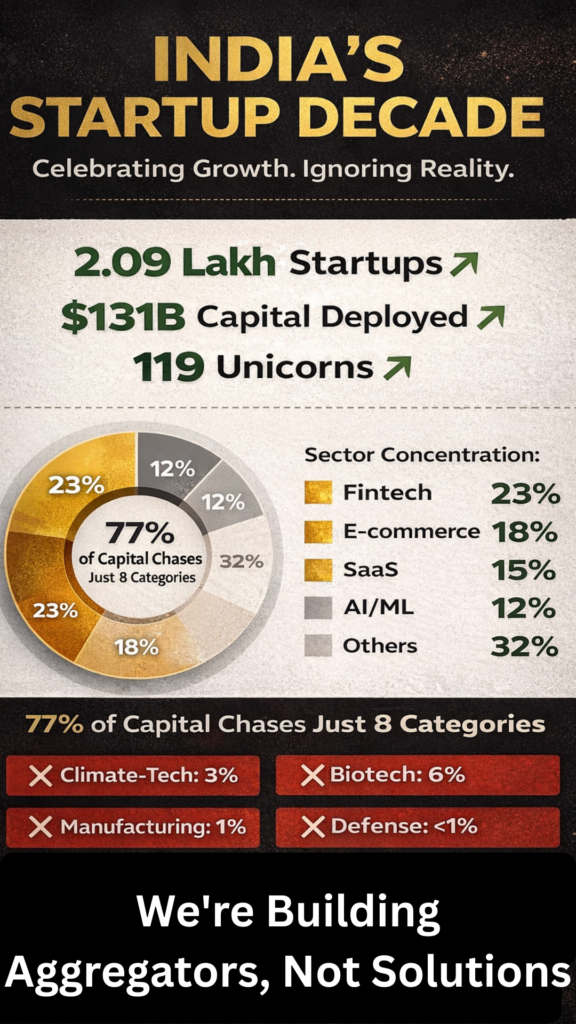

India’s startup ecosystem achieved the impossible: 2.09 lakh recognized startups, 1.66 million jobs, $131 billion raised, 119 unicorns. Yet beneath these spectacular numbers lies a structural fragility that threatens the ecosystem’s long-term relevance.

On January 16, 2026, as India celebrated a decade of Startup India, few noticed the uncomfortable truth: the ecosystem has optimized for speed and scale, not impact and resilience. It is a story of aggregators and quick exits, not deep innovation. And it must change.

The Aggregator Trap: Why India is Building Copies, Not Breakthroughs

Walk into any venture capital office in Bengaluru, and you will hear the same pitch: fintech, e-commerce, SaaS, logistics. These four categories account for 68% of all startup capital deployed in India. Fintech alone—payment systems, lending platforms, investment apps—captures 23% of all startup ecosystem attention. E-commerce, another 18%.

This is rational from a venture capital perspective. Fintech and e-commerce solve immediate market problems in a cash-heavy, underbanked economy. The unit economics are clear: customer acquisition costs are predictable, lifetime value is calculable, and exit markets exist (Google Pay, Amazon, Jio, Flipkart). A founder with a good payment gateway or D2C brand can scale to Series B in 18 months.

But this is the path of aggregation, not innovation.

India’s fintech startups—however successful (Razorpay, Zerodha)—are ultimately building infrastructure that intermediates existing financial flows. They extract value through commissions and data, but they do not fundamentally create new value. They are margin traders, not technologists.

Contrast this with China’s startup ecosystem, where the government’s deliberate shift toward semiconductor manufacturing, AI, and biotech has forced capital and talent concentration into genuinely innovative sectors. Or the U.S., where deep-tech startups in energy, materials science, and climate technology have attracted patient capital precisely because they solve existential problems.

India’s startups, by contrast, are optimizing for speed: product-market fit in 6 months, Series A in 18 months, exit in 3-5 years. This is venture capital’s definition of success. It is not the definition of structural economic transformation.

The Missing Sectors: Where India’s Startup Ecosystem Fails

Consider India’s actual structural problems:

1. Climate & Sustainability: Only 3-4% of startup capital flows to climate-tech. Yet India faces a $2.5 trillion climate adaptation challenge by 2030. Where are the startups solving agricultural resilience, water scarcity, renewable energy storage, and waste-to-value? A handful exist (Takachar, Uravu Labs), but they languish for capital because they require manufacturing partnerships, regulatory approval, and 5-10 year development timelines—all anathema to venture capital’s playbook.

2. Healthcare & Biotech: Only 6% of startups. India manufactures 50% of the world’s vaccines, yet almost no Indian startup is attempting to build drug discovery platforms, diagnostic innovation, or personalized medicine at scale. The exception (Zepto-style rapid delivery) is logistics, not science.

3. Advanced Manufacturing & Materials Science: Virtually absent. India is the world’s second-largest manufacturer, yet its startups are not innovating in precision engineering, advanced materials, or Industry 4.0 automation. Why? Because manufacturing requires capital intensity, long development cycles, and technical depth that venture capital has trained founders to avoid.

4. Defense & Aerospace Technology: Only 2% of startups. India spends $65 billion annually on defense, yet almost no indigenous startup ecosystem exists to innovate in defense tech, drones, and aerospace. The government is trying to correct this (INDiA Stack initiatives), but five years too late.

5. Deep-Tech Agriculture: Minimal capital. India’s farming community faces challenges in soil health, precision input management, and climate-adaptive crop selection. AgriTech startups exist, but they optimize for logistics (Ninjacart) rather than innovation (genetic improvement, soil mapping, sensor networks).

The pattern is unmistakable: India’s startup ecosystem is a cash-flow optimization machine, not a problem-solving institution.

The Critique: What Policymakers Must Demand

Policy Scope #1: Sectoral Capital Mandates

The Rs 1 lakh crore R&D fund announced by the government must have hard allocation targets: minimum 25% to climate-tech, 15% to biotech/healthcare innovation, 20% to advanced manufacturing, 10% to defense-tech. Leaving allocation to “market forces” ensures the money flows to fintech Series C rounds.

Policy Scope #2: Long-Duration Capital Instruments

Deep-tech requires 10-15 year investment horizons. Venture capital operates on 7-year fund cycles. The solution: government-backed development finance institutions (like Singapore’s Temasek or Korea’s state funds) investing in patient capital vehicles specifically for deep-tech.

Policy Scope #3: Manufacturing Incubation Hubs

Instead of 244 software incubators, establish 50 advanced manufacturing incubators with access to fabrication equipment, prototype funding, and industry partnerships. The marginal cost is higher, but the impact is transformative.

Policy Scope #4: Founder Diversity Beyond Gender

The focus on women entrepreneurs is essential, yet insufficient. The real gap is sectoral diversity of founder backgrounds: Where are the scientists, engineers, and domain experts leaving research institutions to build deep-tech startups? Incentivize sabbaticals for academic researchers to found startups; provide IP ownership clarity.

The Call: From Aggregation to Impact

India’s next decade must ask not “how many startups?” but “how many solutions?” The ecosystem’s maturity is measured not by unicorn valuations but by the fraction of India’s structural problems being solved by Indian startups.

Celebrating 2.09 lakh startups while 77% of capital chases just 8 categories is not success. It is the illusion of success.

The real National Startup Day begins when a climate-tech startup achieves $1 billion valuation, when a biotech founder declines a fintech acquisition offer, when a defense-tech startup is India’s next household name.

Until then, we are not innovating. We are intermediating.